Apple ships 71.7m smartphones in Q4 2018 as global market falls 6%

Palo Alto, Shanghai, Singapore and Reading (UK) – Tuesday, January 29 2019

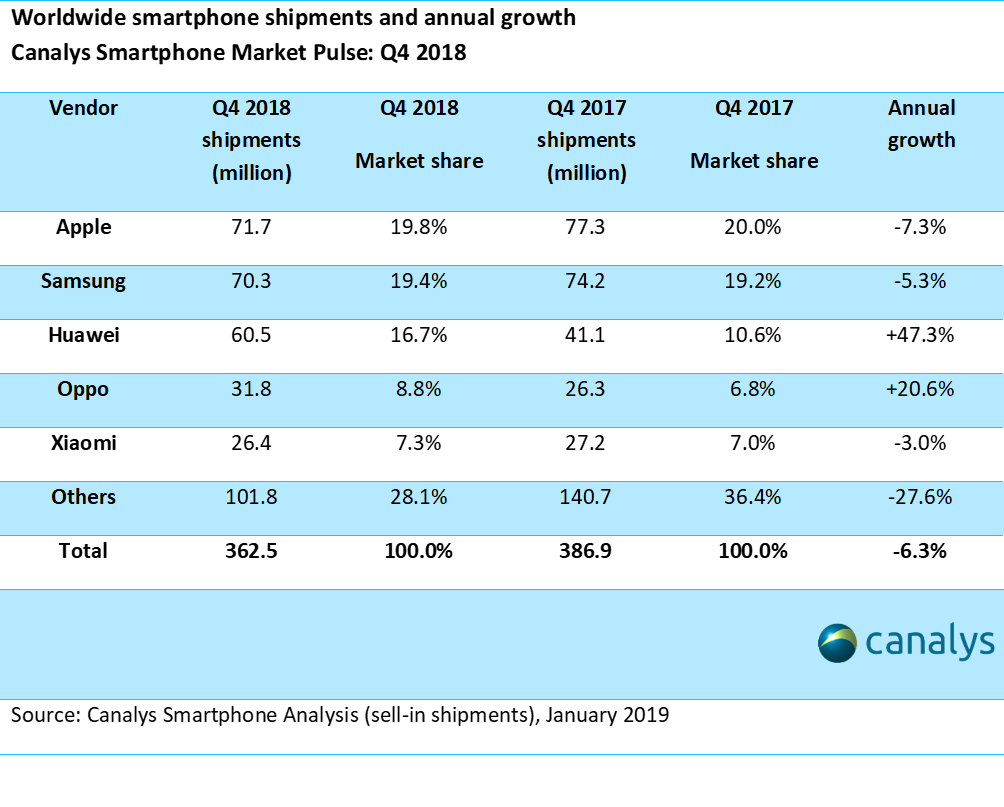

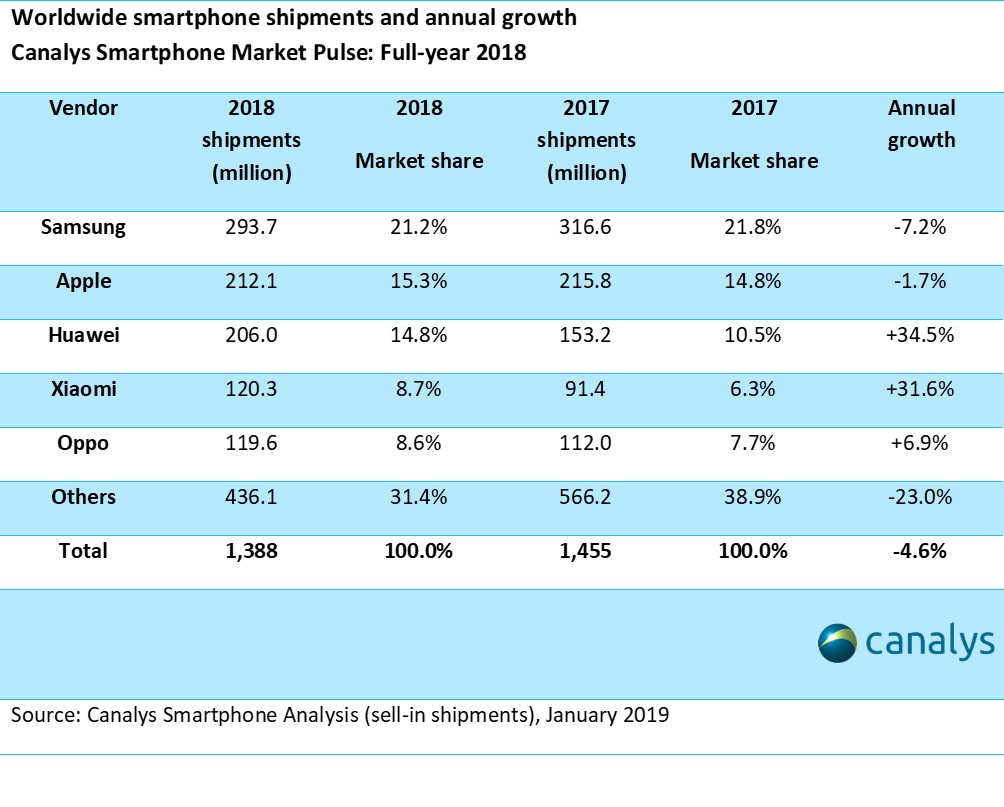

The global smartphone market declined for the fifth consecutive quarter, falling 6% to 362 million in Q4 2018. Apple overtook Samsung to become the largest vendor in Q4, shipping 71.7m units of iPhone. Huawei, Oppo and Xiaomi completed the top five vendors. For the full-year 2018, global smartphone shipments totaled 1.4 billion, down 5% from 1.5 billion in 2017.

“It is no shock to smartphone vendors that the market has passed its peak,” said Senior Analyst Ben Stanton, “People are clearly keeping phones for longer as product innovation slows. But the speed and severity of shipment decline has caught many vendors, investors, and other companies in the value chain off guard. International factors like the US-China trade war, weak consumer spending in developed markets, and a buoyant market for refurbished phones, have catalyzed the decline of smartphone shipments."

Vendor Highlights:

Apple iPhone shipments were down 7% over Q4 2017, falling short of its own expectations, but it still took the number one position in Q4 2018. The iPhone XR with over 22 million shipments was the top shipping iPhone, and has emerged as a model which Apple seems particularly flexible about discounting. This was followed by iPhone XS Max and iPhone XS, which shipped over 14 million and 9 million units respectively. Apple completed the full-year in second place, and it has major challenges ahead in 2019 as its core markets, particularly China, continue to decline. Apple will focus intently on growing its services revenue, relying now on its sticky installed base of users. But with vendors like Samsung and Huawei providing cheaper and competitive alternative devices, Apple may need to launch a cheaper iPhone, or at least become more flexible with channel discounting, to safeguard the same installed base it has bet its future on.

Samsung fell to second position in Q4 2018, after a 5% decline in its shipments to 70.3 million units. It was a humbling year for Samsung in 2018, as it succumbed to hyper-aggressive price competition by Huawei, Xiaomi, Oppo and Vivo, especially in Asia and Europe. It shipped 23 million fewer devices than in 2017, and its full-year total of 294 million units fell significantly short of its 320 million target. But this has roused the Korean vendor, and caused it to overhaul its smartphone strategy, which now focuses on sacrificing hardware margin to pack more technology into low-end and mid-range phones. 2019 will see Samsung fight back and gain lost share from the likes of Huawei, Oppo, Vivo and Xiaomi.

Huawei, in contrast, had a stunning 2018, which was topped off with 47% growth to 60.5 million units in Q4. It took record market share in China (see Canalys press release “China’s smartphone market falls 14% in 2018, with just under 400 million units shipped”), but its real growth engine was overseas, where it increased shipments by more than 60%. Huawei demonstrated tangible technology leadership in 2018, pioneering features such as its triple lens AI-enhanced camera, which helped transform its brand perception in overseas markets. Its new image as a technology leader has helped Huawei increase shipments across all price points. However, moving into 2019, it now faces a critical challenge, as political tensions, security concerns and disputes over intellectual property theft threaten to disrupt its remarkable momentum. Any major impact on Huawei’s enterprise and carrier business will ripple through the organization and affect the smartphone business.

For more information, please contact:

Canalys EMEA: +44 118 984 0520

Ben Stanton: ben_stanton@canalys.com +44 118 984 0525

Kelly Wheeler: kelly_wheeler@canalys.com +44 118 984 0529

Canalys APAC (Shanghai): +86 21 2225 2888

Nicole Peng: nicole_peng@canalys.com +86 21 2225 2815

Mo Jia: mo_jia@canalys.com +86 21 2225 2812

Canalys APAC (Singapore): +65 6671 9399

Rushabh Doshi: rushabh_doshi@canalys.com +65 6671 9387

Shengtao Jin: shengtao_jin@canalys.com +65 6657 9303

Canalys Americas: +1 650 681 4488

Vincent Thielke: vincent_thielke@canalys.com +1 650 656 9016

Marcy Ryan: marcy_ryan@canalys.com +1 650 681 4487

About Canalys

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

Receiving updates

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please complete the contact form on our web site.

Alternatively, you can email press@canalys.com or call +1 650 681 4488 (Palo Alto, California, USA), +65 6671 9399 (Singapore), +86 21 2225 2888 (Shanghai, China) or +44 118 984 0520 (Reading, UK).