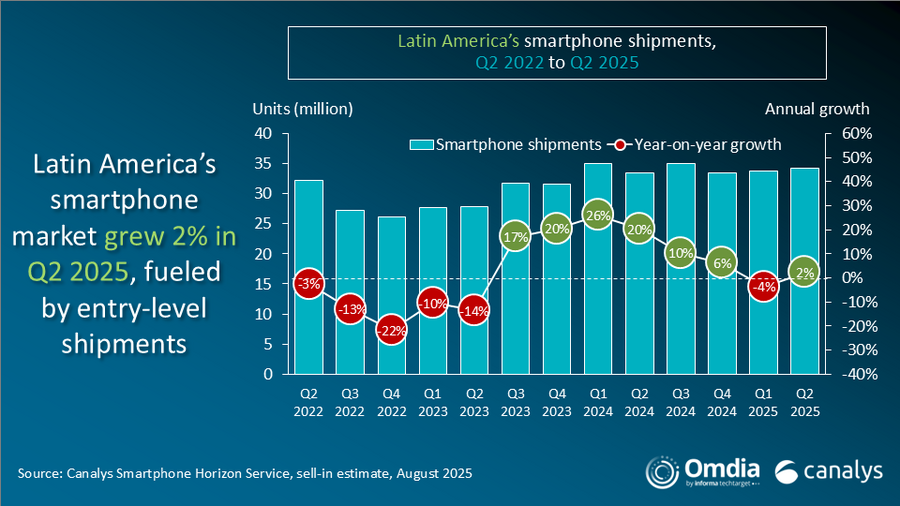

Europe’s smartphone market fell 9% in Q2 2025, as eco-design regulations came into force

Thursday, 28 August 2025

TechTarget and Informa Tech’s Digital Business Combine

TechTarget and Informa Tech’s Digital Business CombineWith a combined permissioned audience of 50+ million professionals, TechTarget and Informa Tech’s digital businesses have come together to offer industry-leading, global solutions that enable vendors in enterprise technology and other key industry markets to accelerate their revenue growth at scale.

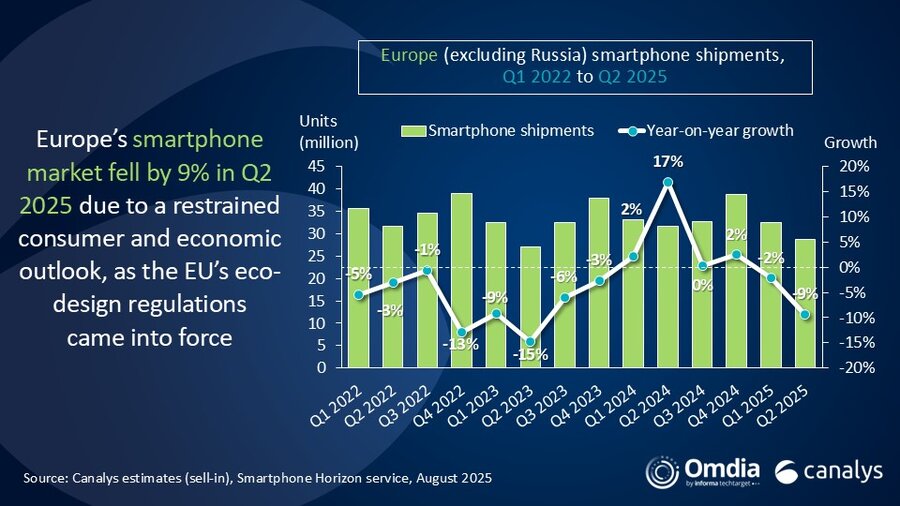

Smartphone shipments into Europe (excluding Russia) fell by 9% to 28.7 million units in Q2 2025, according to Canalys (now part of Omdia). A restrained consumer and economic outlook is still limiting demand, making Europe the worst-performing smartphone region worldwide in Q2.

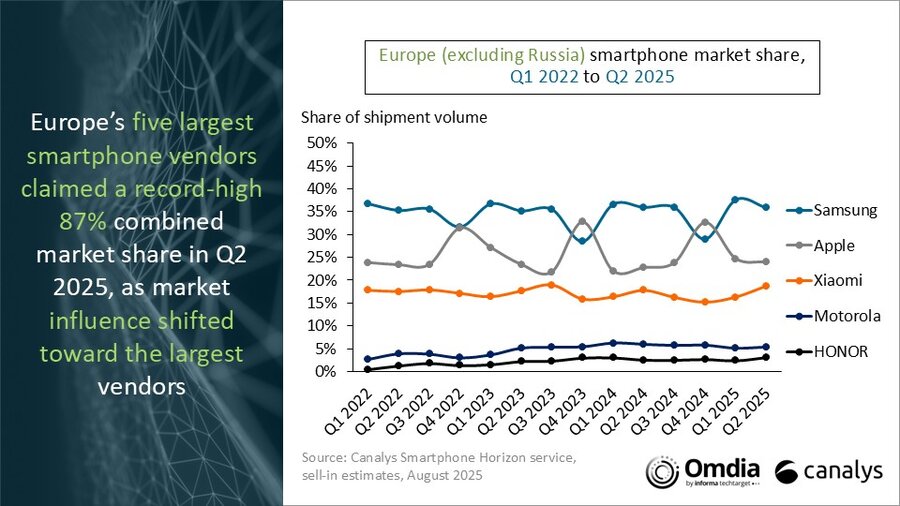

On the vendor ranking table, Samsung sustained a confident lead, despite declining 10% year on year to 10.3 million units. Its volume performance was hurt by the Galaxy A06 not being brought into EU-regulated markets due to eco-design regulations. Apple was the second largest vendor, declining by 4% to 6.9 million units. A consistent iPhone 16 series performance partly helped offset a slimmer portfolio covering fewer price segments than in Q2 2024. Xiaomi finished third, declining by 4% to 5.4 million units. Its strong comeback in Italy, where it grew more than 50% year on year, helped balance out an overall tough demand environment. Motorola and HONOR rounded out the top five, respectively declining 18% and growing 11% to 1.5 million and 0.9 million units.

“Players in Europe’s smartphone industry have had a tough first half of 2025, defined by sluggish end-user demand and conservative channel inventory strategies,” said Aaron West, Senior Analyst at Omdia. “Additionally, the EU eco-design and energy efficiency regulations came into force in late June, which vendors have spent years preparing for. Any vendors’ desire to stockpile channel inventory ahead of 20 June failed to materialize as the channel remained resistant to taking on any excess inventory. Plus, some of the largest network operators required devices in their portfolios to be compliant a few months in advance. But a healthy channel dynamic positions the market for growth in the second half of the year, as industry players strive to get a positive return on the momentum from the major launch events.”

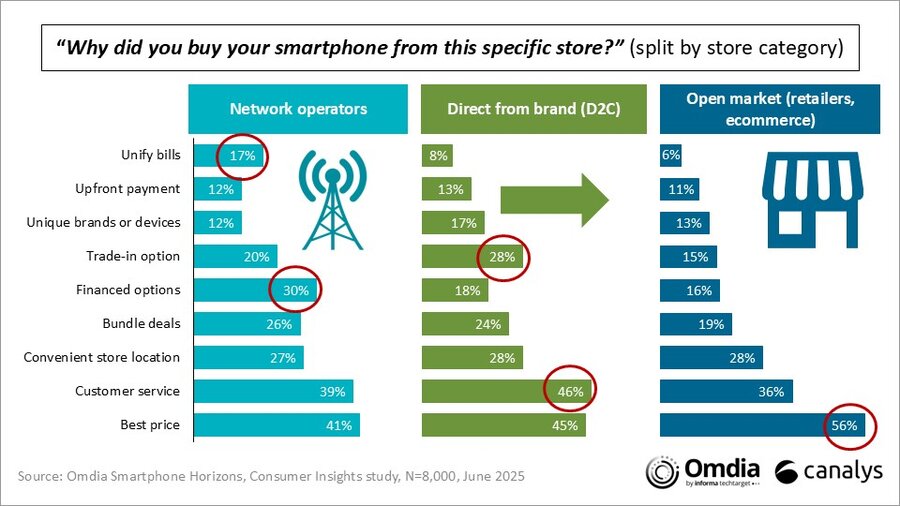

“Market influence continues to shift toward the largest five players, which held a record-high 87% combined market share in Q2 2025,” said Runar Bjørhovde, Senior Analyst at Canalys (now part of Omdia). “While it reflects the importance of differentiated brands and scale for a profitable and sustainable business model for vendors, competition remains brutally fierce within the channel. Here, telcos, retailers, e-commerce specialists and direct channels (D2C) are all competing intensely to acquire and retain customers. But growing dependence on a few vendors is making it hard to differentiate. In recent years, both D2C and open-market channels have taken some share, mainly from operators. Our recent consumer study of 8,000 Europeans found that the draw toward direct purchases relates to a desire to engage with the brand alongside perceived customer service, while the draw to open-market channels largely relates to pricing. Operators remain a key route to the market for vendors and have been a key catalyst to drive adoption of, for example, 5G and eSIM capable smartphones.”

|

Europe (excluding Russia) smartphone shipments and annual growth |

|||||

|

Vendor |

Q2 2025 |

Q2 2025 |

Q2 2024 |

Q2 2024 |

Annual |

|

Samsung |

10.3 |

36% |

11.3 |

36% |

-10% |

|

Apple |

6.9 |

24% |

7.2 |

23% |

-4% |

|

Xiaomi |

5.4 |

19% |

5.6 |

18% |

-4% |

|

Motorola |

1.5 |

5% |

1.9 |

6% |

-18% |

|

HONOR |

0.9 |

3% |

0.8 |

3% |

11% |

|

Others |

3.7 |

13% |

4.8 |

15% |

-22% |

|

Total |

28.7 |

100% |

31.6 |

100% |

-9% |

|

|

|

|

|||

|

Note: percentages may not add up to 100% due to rounding |

|

||||

Aaron West: aaron.west@omdia.com

Runar Bjørhovde: runar_bjorhovde@canalys.com

The worldwide Smartphone Horizon service from Canalys (now part of Omdia) provides a comprehensive country-level view of shipment estimates far in advance of our competitors. We provide quarterly market share data, timely historical data tracking, detailed analysis of storage, processors, memory, cameras and many other specs. We combine detailed worldwide statistics for all categories with Canalys’ unique data on shipments via tier-one and tier-two channels. The service also provides a unique view of end-user types. At the same time, we deliver regular analysis to give insights into the data, including the assumptions behind our forecast outlooks.

Canalys, now part of Omdia, is a leading global technology market analyst firm with a distinct channel focus. We strive to guide clients on the future of the technology industry and to think beyond the business models of the past. We’ve delivered market analysis and custom solutions to technology vendors worldwide for over 25 years. Our research covers emerging, enterprise, mobile and smart technologies. Understanding channels is at the heart of everything we do. Our insightful reports, data and forecasts inform our clients’ strategies, while the Canalys Forums and Candefero online community give the channel feedback opportunities. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please contact us. Alternatively, you can email press@canalys.com.

Please click here to unsubscribe

Copyright © 2025 TechTarget, Inc. or its subsidiaries. All rights reserved.