Global cloud spending surged 21% in Q1 2025

Thursday, 12 June 2025

TechTarget and Informa Tech’s Digital Business Combine

TechTarget and Informa Tech’s Digital Business CombineWith a combined permissioned audience of 50+ million professionals, TechTarget and Informa Tech’s digital businesses have come together to offer industry-leading, global solutions that enable vendors in enterprise technology and other key industry markets to accelerate their revenue growth at scale.

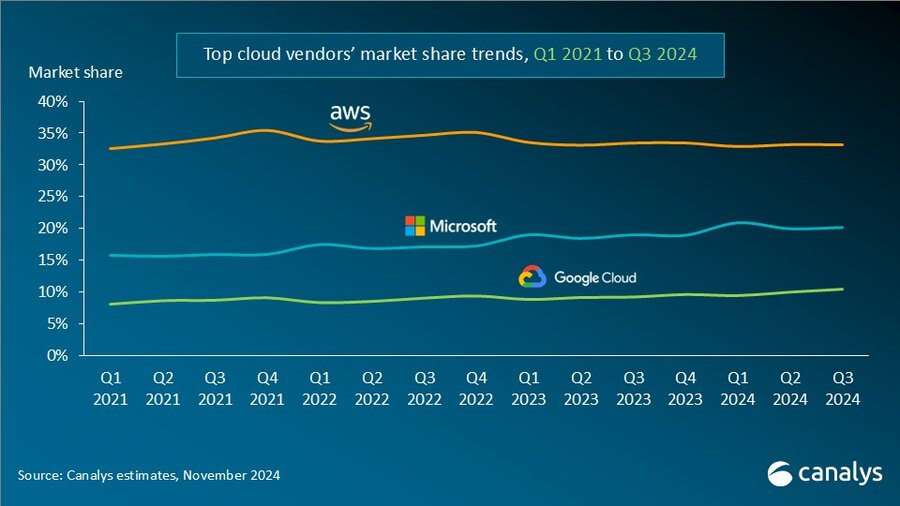

Global spending on cloud infrastructure services, according to Canalys (now part of Omdia) estimates, reached US$90.9 billion in Q1 2025, marking a 21% year-on-year increase. Enterprises have recognized that deploying AI applications requires renewed emphasis on cloud migration. Large-scale investment in both cloud and AI infrastructure remains a defining theme of the market in 2025. Meanwhile, to accelerate the enterprise adoption of AI at scale, leading cloud providers are intensifying efforts to optimize infrastructure—most notably through the development of proprietary chips—aimed at lowering the cost of AI usage and improving inference efficiency. In Q1 2025, the ranking of the top three cloud providers (AWS, Microsoft Azure, and Google Cloud) remained unchanged from the previous quarter, with their combined market share accounting for 65% of global cloud spending. Collectively, the three hyperscalers recorded a 24% year-on-year increase in cloud-related spending.

Growth momentum diverged among the top players. Microsoft Azure and Google Cloud both maintained growth rates of over 30% (although Google Cloud’s growth slowed slightly from the previous quarter), while AWS grew by 17%, a deceleration from 19% growth in Q4 2024. This deceleration was largely driven by supply-side constraints, which limited the ability to meet rapidly rising AI-related demand. In response, cloud hyperscalers have continued to invest aggressively in AI infrastructure to expand capacity and position themselves for long-term growth.

Overall, the global cloud services market sustained steady growth in Q1 2025, as enterprises sharpened their focus on two strategic priorities: accelerating cloud migration—either by shifting additional workloads or reviving stalled on-premises transitions—and exploring the adoption of generative AI. The rise of generative AI, which relies heavily on cloud infrastructure, has in turn reinforced enterprise cloud strategies and hastened migration timelines.

“As AI transitions from research to large-scale deployment, enterprises are increasingly focused on the cost-efficiency of inference, comparing models, cloud platforms, and hardware architectures such as GPUs versus custom accelerators,” said Rachel Brindley, Senior Director at Canalys (now part of Omdia ). “Unlike training, which is a one-time investment, inference represents a recurring operational cost, making it a critical constraint on the path to AI commercialization.”

“Many AI services today follow usage-based pricing models—typically charging by token or API call—which makes cost forecasting increasingly difficult as usage scales,” added Yi Zhang, Analyst at Canalys (now part of Omdia ). “When inference costs are volatile or excessively high, enterprises are forced to restrict usage, reduce model complexity, or limit deployment to high-value scenarios. As a result, the broader potential of AI remains underutilized.”

To address these challenges, leading cloud providers are deepening their investments in AI-optimized infrastructure. Hyperscalers including AWS, Azure, and Google Cloud have introduced proprietary chips such as Trainium and TPU, and purpose-built instance families, all aimed at improving inference efficiency and reducing total cost of AI.

Amazon Web Services (AWS) maintained its position as the market leader in Q1 2025, capturing 32% of global market share and recording a 17% year-over-year increase in revenue. Its AI business continues to grow at a triple-digit annual rate, though it remains in the early stages of development. In March, AWS introduced a price-cutting strategy to promote adoption of its Trainium AI chips over more costly NVIDIA-based solutions, highlighting Trainium 2’s 30–40% price-performance advantage. The company also accelerated the expansion of its Bedrock service, adding Anthropic’s Claude 3.7 Sonnet and Meta’s Llama 4 models, and became the first cloud provider to fully manage DeepSeek R1 and Mistral’s Mixtral Large. Further underscoring its long-term commitment to global infrastructure, AWS announced a capital investment of over US$4 billion in May 2025 to establish a new cloud region in Chile by the end of 2026.

Microsoft Azure remained the second-largest cloud provider in Q1 2025, holding a 23% market share and delivering strong year-over-year growth of 33%. Microsoft reported a 16 point growth rate lift to Azure from AI, marking the largest single-quarter uplift since Q2 2024. In April, Azure announced the availability of the GPT-4.1 model series on both Azure AI Foundry and GitHub, further broadening developer access to advanced AI capabilities across its ecosystem. Azure AI Foundry, Microsoft’s platform for building and managing AI applications and agents, is now used by developers at more than 70,000 enterprises. The platform processed over 100 trillion tokens this quarter, a fivefold increase year-over-year. Microsoft has also focused on lowering the cost of AI adoption, reporting a nearly 30% improvement in its AI performance at constant power consumption and a reduction of over 50% in cost per token. As part of its ongoing global infrastructure expansion, it opened new data centers in 10 countries across four continents during Q1.

Google Cloud, the world’s third-largest cloud provider, maintained a 10% market share in Q1 2025 and delivered strong year-over-year growth of 31%. As of 31 March, its revenue backlog reached US$92.4 billion, marking a slight decline from the previous quarter. This decrease was primarily attributed to supply constraints, particularly in compute capacity, that limited Google Cloud’s ability to fully meet customer demand. In March, Google introduced the Gemini 2.5 model series, with Gemini 2.5 Pro receiving widespread acclaim for its leading benchmark performance and top ranking on Chatbot Arena. With enhanced reasoning and coding capabilities, the model opens new possibilities for both developers and enterprise users. Since the beginning of the year, active usage of Google AI Studio and the Gemini API has surged by over 200%, reflecting strong developer adoption and growing demand for generative AI solutions. Google also launched a new cloud region in Sweden (its 42nd globally) and committed US$7 billion to expand its Iowa data center, further supporting its growing AI and cloud workloads.

For more information, please contact:

Rachel Brindley: rachel_brindley@canalys.com

Yi Zhang: yi_zhang@canalys.com

Canalys, now part of Omdia, is a leading global technology market analyst firm with a distinct channel focus. We strive to guide clients on the future of the technology industry and to think beyond the business models of the past. We’ve delivered market analysis and custom solutions to technology vendors worldwide for over 25 years. Our research covers emerging, enterprise, mobile and smart technologies. Understanding channels is at the heart of everything we do. Our insightful reports, data and forecasts inform our clients’ strategies, while the Canalys Forums and Candefero online community give the channel feedback opportunities. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please contact us. Alternatively, you can email press@canalys.com.

Please click here to unsubscribe

Copyright © 2025 TechTarget, Inc. or its subsidiaries. All rights reserved.