Worldwide cloud service spending to grow by 20% in 2024

Monday, 26 February 2024

Canalys is part of Informa PLC

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC’s registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

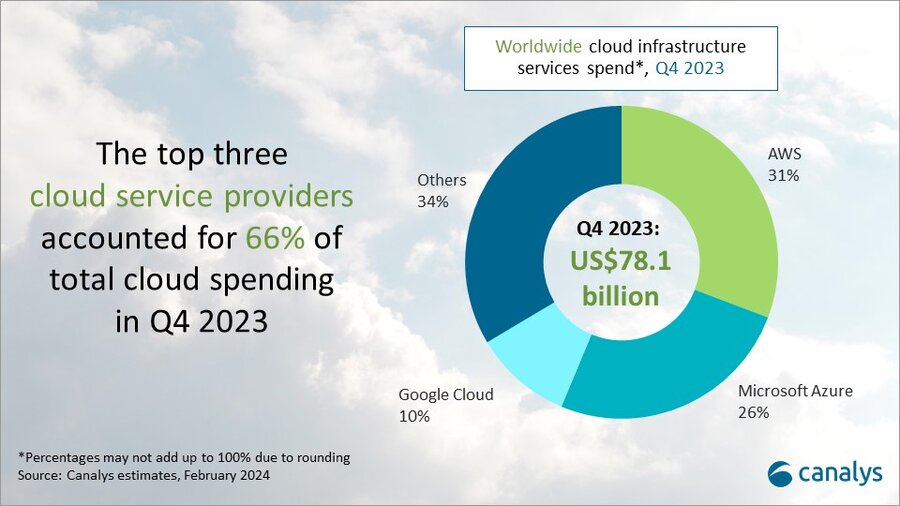

Worldwide cloud infrastructure services expenditure grew 19% year on year in Q4 2023 to reach US$78.1 billion, an increase of US$12.3 billion. For full-year 2023, total cloud infrastructure services spending grew 18% to US$290.4 billion, up from US$247.1 billion in 2022. The influence of enterprise IT optimization on the cloud services market is falling, with more customers expanding their commitments with hyperscalers in anticipation of increased consumption requirements. Cloud migration efforts are picking up again, alongside a surge in new demand, particularly in the widespread adoption of AI applications. Hyperscalers are steadily ramping up investments in generative AI, expecting that harnessing its capabilities will catalyze new opportunities in cloud consumption. In 2024, Canalys expects global cloud infrastructure services spending to increase by 20%, compared with 18% in 2023.

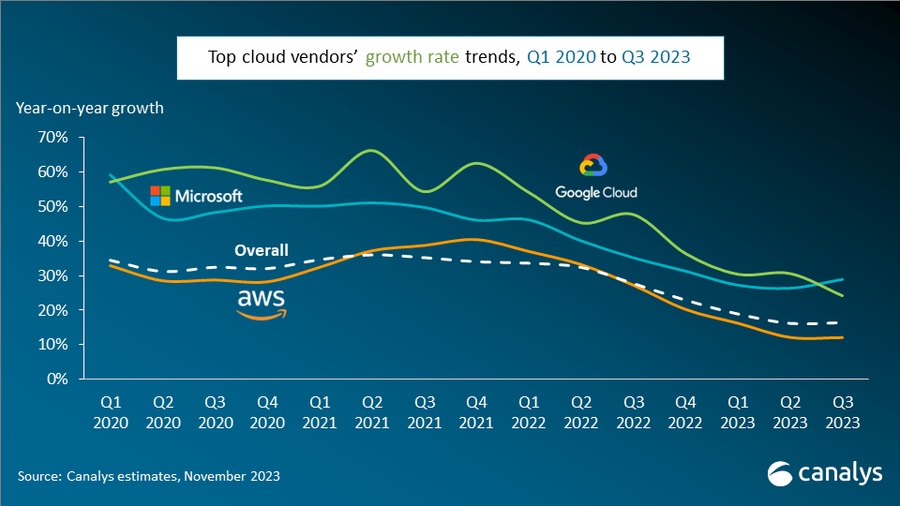

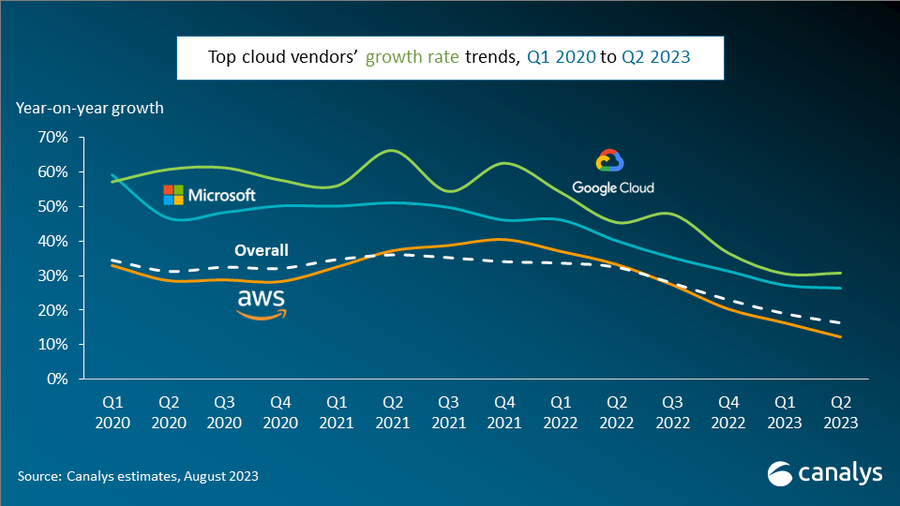

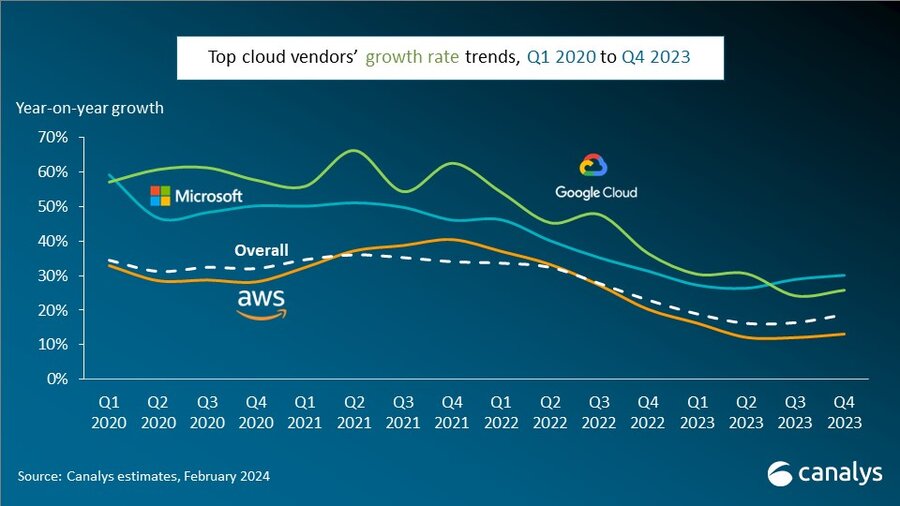

In Q4 2023, the top three cloud providers – AWS, Microsoft Azure and Google Cloud – jointly grew by 21% and accounted for 66% of total spending. In Q4, Microsoft Azure and Google Cloud saw a strong resurgence in revenue growth, both exceeding 25% once again. With 30% growth, Microsoft significantly outpaced the market and continues to close the gap on AWS. Market leader AWS saw an uptick in growth compared with previous quarters, but an increase of 13% year on year remains behind the trajectory of both Microsoft Azure and Google Cloud. “AWS has been slower than its key competitors to make AI advances, which may explain why its growth is not accelerating as rapidly as that of Azure and GCP,” said Yi Zhang, Analyst at Canalys. “The integration of generative AI into mainstream software products is accelerating, potentially leading to quicker commercialization of generative AI applications. Google recently introduced its rebranded Gemini large language model into Workspace applications, such as Gmail and Docs. At the same time, Microsoft launched Copilot for Microsoft 365 last November, embedding its generative AI platform into Word, Excel and other office applications.”

“This trend underscores the growing importance of AI in enhancing user experiences, productivity and efficiency within software ecosystems,” said Alex Smith, VP at Canalys. “As AI continues to evolve, solution providers are exploring integration opportunities beyond vendor offerings, aiming to leverage AI capabilities to innovate and deliver enhanced solutions to their clients.”

Canalys defines cloud infrastructure services as those services that provide infrastructure-as-a-service and platform-as-a-service, either on dedicated hosted private infrastructure or shared public infrastructure. This excludes software-as-a-service expenditure directly but includes revenue generated from the infrastructure services being consumed to host and operate them.

For more information, please contact:

Alex Smith: alex_smith@canalys.com

Yi Zhang: yi_zhang@canalys.com

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please contact us. Alternatively, you can email press@canalys.com.

Please click here to unsubscribe

Copyright © Canalys. All rights reserved.